Daily Forecast

Intraday to 5-day direction probabilities, expected trading ranges, and volatility bands for real-time margin monitoring and intraday collateral calls.

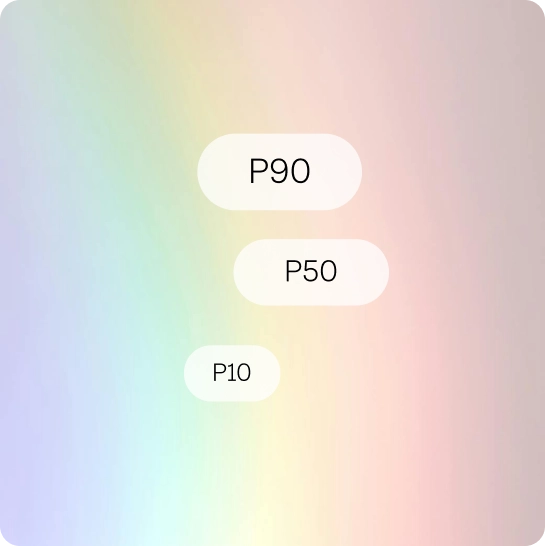

Weekly Forecast

1–13 week forward curves with full P10/P50/P90 confidence intervals, used for weekly mark-to-market and advance-rate adjustments.

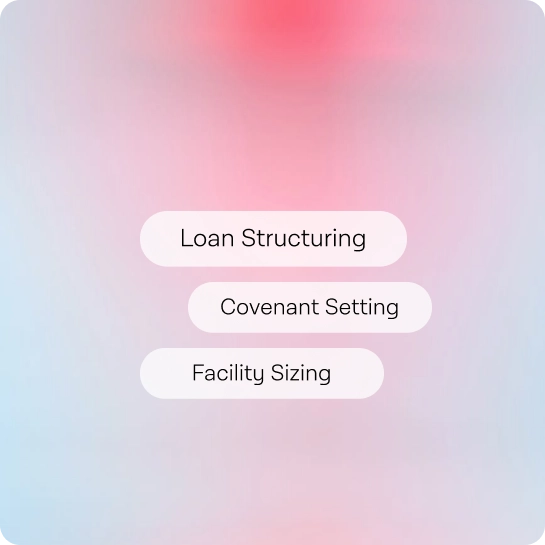

Monthly/Strategic Forecasts

3–36 month probabilistic price decks purpose-built as the primary input for initial loan structuring, covenant setting, and long-term facility sizing.

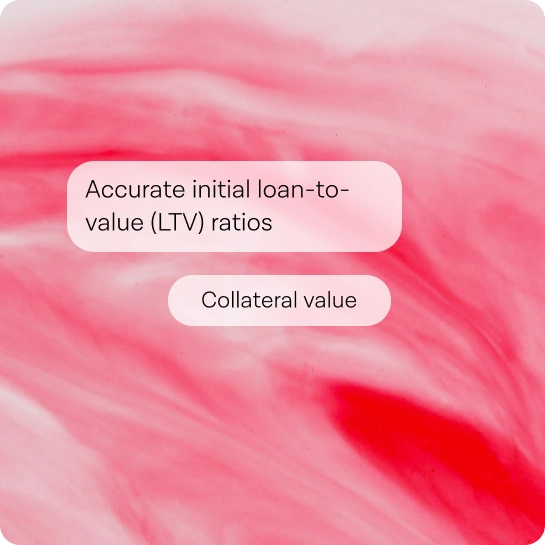

Stress-Test LTV With Forward Price Simulations

Determine accurate initial loan-to-value (LTV) ratios and advance rates by stress-testing collateral value against thousands of realistic future price paths.

Dynamic Borrowing-Base Formulas That Update Automatically

Set dynamic borrowing-base formulas and margin triggers that automatically adjust to the latest forward price probabilities instead of lagging monthly marks.

Scenario-Driven LGD and Default Risk Haircuts

Calculate expected loss-given-default (LGD) and probability-of-default haircuts under multiple downside scenarios, enabling tighter pricing on high-quality deals.

Full-Lifecycle Collateral Coverage Forecasting

Generate forward-looking collateral coverage ratios for the entire life of the facility (6 months to 5+ years), eliminating the chronic under- or over-collateralization that arises from stale pricing decks.

Consistent Pricing Across Commodities and Inventory Types

Rank and price facilities across different commodity types or borrower inventories using a single, consistent forward-price methodology.